Financial Insights

for Professionals

In-depth analysis of Canadian tax strategy, investment architecture, and wealth planning for high-income professionals. No generic advice. No product pitches.

The Red Line Too Many Chinese Canadians Cross: Four CRA Audit Triggers

For many Chinese Canadians, tax season ends not with relief but with quiet anxiety. The CRA's audit system is not random — it operates on a sophisticated algorithm that flags logical inconsistencies. This article examines four red lines disproportionately crossed by members of the Chinese Canadian community: chronic business losses, unreported small income slips, frequent trading reclassified as business income, and undisclosed foreign assets.

From Employee to Entrepreneur: The Case for Building a Corporation in Canada

Relying solely on T4 employment income in Canada means handing nearly half your earnings to the CRA before you see a dollar. This article breaks down the three core advantages of incorporating a small business: the tax rate arbitrage between personal and corporate rates, the ability to deduct business expenses before tax, and the LCGE — a lifetime exemption of over $1 million in capital gains when you eventually sell.

CRA's Hidden Audit Algorithm: Four Red Lines That Trigger a Tax Review

The CRA's audit system is not a random lottery. It operates on a sophisticated risk-scoring algorithm designed to detect logical inconsistencies in tax filings. This article examines four of the most common triggers: chronic business losses, unreported small income slips, frequent trading reclassified as business income, and undisclosed foreign assets.

The Magic of Borrowing: How to Push Inflation Risk Back to the Bank

Every dollar the bank lends you is quietly working in your favour. The true power of investment loans lies in systematically transferring inflation risk back to the bank — letting time and monetary erosion work for you, not against you.

2026 Canadian Financial Truth: Why I Advise You "Don't" Save in a TFSA?

Stop foolishly saving in TFSAs! 90% of people are using them wrong. This is an investment tool, not a piggy bank! Unveiling 3 common misconceptions that turn tax-free accounts into tax abysses.

Three Advanced TFSA Strategies Your Bank Manager Will Never Tell You

Same contribution room, vastly different outcomes — some accounts sit at $20,000 after three decades while others grow to nearly $1,000,000. The difference isn't luck. It's strategy.

Canada Pension Plan (CPP) Guide: Why Chinese Immigrants Should Plan Their Own Retirement

Living in Canada, many Chinese immigrants are frustrated by the mandatory CPP (Canada Pension Plan) deductions from their monthly paychecks. As a nationwide compulsory public pension system,

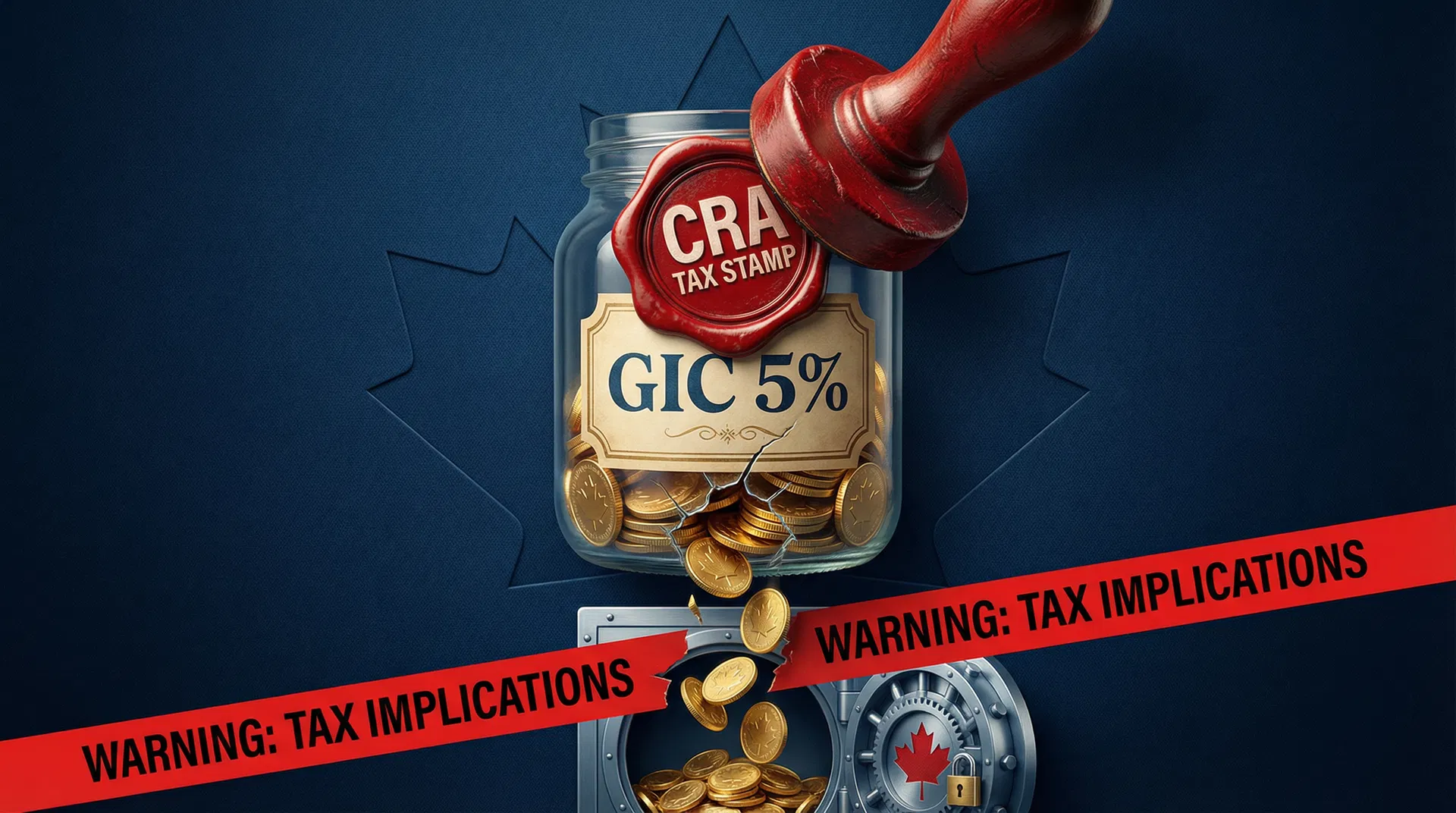

You're Not Earning 5% on Your GIC. The CRA Is.

Think GIC is the safest investment? One client put $500K into a GIC, earned $25K in interest—and walked away with just $14K. The CRA quietly took nearly half. This isn't a GIC problem. It's a placement problem.

Stop spending money to "buy" a job!

"In Canada, the biggest fear is spending money to buy a job" (A sharp critique of the pain points of the Chinese community, exposing the cruel truth of "pseudo-entrepreneurship")

Is Your RRSP Working Against You in Retirement?

Most Canadians know that contributing to an RRSP reduces their taxable income today. Far fewer have thought carefully about what happens on the other end. This article outlines the most common RRSP withdrawal mistakes and two key strategies to ensure your retirement savings actually work in your favour.

Top Wisdom for Surviving and Thriving in Canada: The Mindset Shift from "Employee" to "Middleman"

Let me give you some advice: If you live in Canada and only rely on working a traditional job, it will be extremely difficult to turn your life around. Therefore, do not hesitate—you must learn to become a "middleman" (or entrepreneur) in Canada.

Canada Tax Planning 2025: The Complete Guide for High-Income Professionals

Complete guide to RRSP/TFSA maximization, capital gains optimization, corporate structures, and income splitting strategies for professionals earning $150K+.

50,000+ Professionals Follow

Our Financial Education Content

Wallace Wang is one of Canada's most-followed Chinese-language financial educators, with content covering tax strategy, investment planning, and wealth building for high-income professionals. Follow on WeChat, Xiaohongshu, and YouTube for weekly insights.

Frequently Asked Questions

Do I need a financial advisor if I already have a bank advisor?

Bank advisors are limited to their institution's product shelf and are compensated to sell those products. An independent CFP® has access to the full market and a fiduciary obligation to act in your best interest. For high-income professionals, the difference in outcomes is typically significant.

What is the minimum asset level to work with Wallace Wang Financial Services?

We typically work with clients with investable assets above $300,000, or high-income professionals with the capacity to build to that level within 3–5 years. Our focus is on clients where comprehensive financial planning creates meaningful value.

How are you compensated?

We operate on a fee-based model. We receive compensation from product providers when we place insurance or investment products, and we disclose all compensation transparently. We do not charge additional planning fees on top of product compensation.

How often will we meet?

New clients typically have 3–4 meetings in the first year to establish the financial plan and implement strategies. Ongoing clients meet annually for a comprehensive review, with additional meetings as needed for significant life events or market changes.

Do you work with clients outside of Alberta?

Yes. We are licensed in Alberta and British Columbia, and serve clients throughout Western Canada. Most ongoing client meetings are conducted virtually.

What makes your approach different from other financial advisors?

We specialize in a specific client profile — high-income Canadian professionals — and we focus on structure over products. We do not recommend investments or insurance products until we have built a comprehensive financial architecture. Most advisors do the opposite.